By Chuck Penner, LeftField Commodity Research

March 2026

The release of Statistics Canada’s (StatCan) first look at acreage for the upcoming season is usually highly anticipated (by some of us) but is also frequently questioned (also by us). The estimates are based on a farmer survey conducted in mid-December to mid-January, which raises the possibility that results are already outdated by March. While it is true that farmers can change plans and shift acres from one crop to another, a lot of the crop rotation is already decided at that point. This means some changes will show up in the final acreage estimates in June, but they will not be huge.

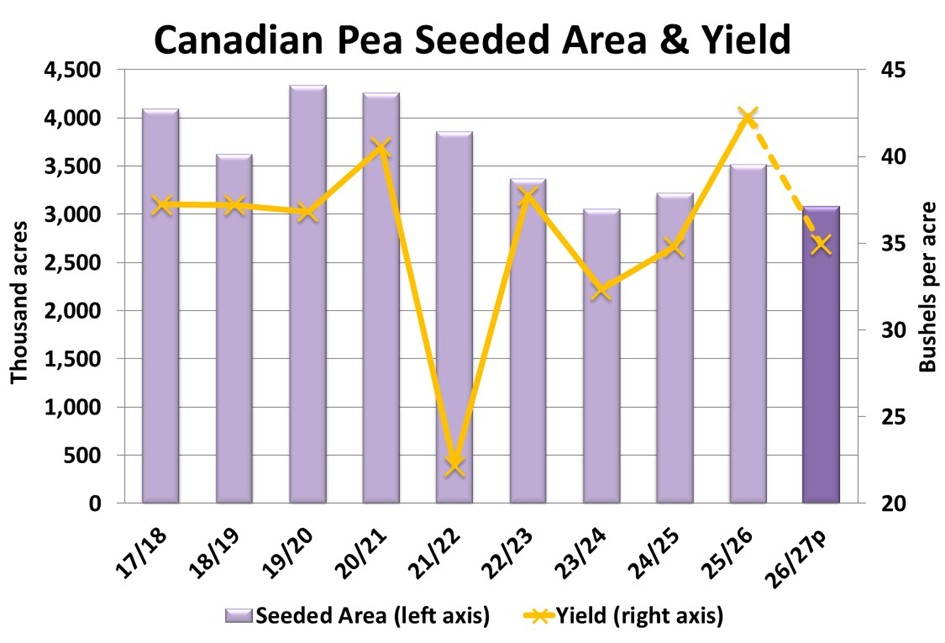

For peas, StatCan estimated 2026 seeded area at 3.08 million acres, down 12% from last year and lower than the five-year average of 3.4 million acres. This decline was not really surprising as frontline feedback was already pointing in that direction. Keep in mind, this survey was conducted prior to the announcement that China was dropping its 100% import tariff on Canadian peas. It is quite possible a few acres will be added back into the 2026 total.

Of course, the pea market is made up of several distinct parts, and how acres will be divided between the various classes is important. Green and maple pea prices are still at a premium to yellow peas in the old-crop market, but there is not the same advantage when it comes to new-crop bids. As a result, there is a good chance seeded area of yellow peas will not shrink as much as other types.

On its own, fewer acres of peas would already result in lower 2026/27 supplies, but yields could play an even larger role. Last year’s yield of 42.3 bushels per acre (bu/acre) was a near record while the average is considerably lower, closer to 35 bu/acre. A repeat of last year’s high yield would be great, but the highest odds are around an average yield. A combination of fewer acres and a return to average yields would mean the 2026/27 pea crop would drop below 2.9 million tonnes, a full million tonnes less than last year. This would help bring next year’s pea supplies back down to more normal levels.

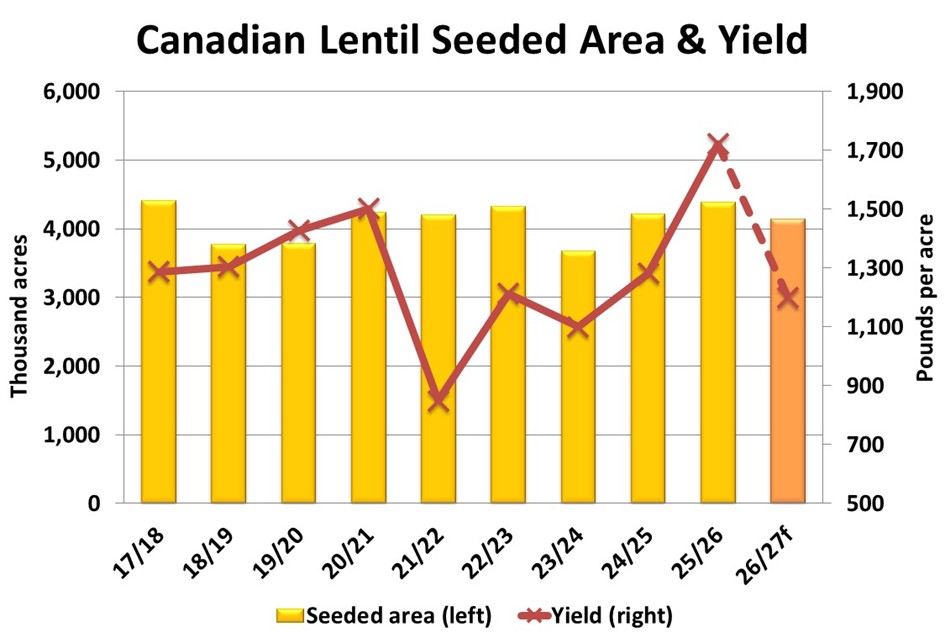

StatCan’s forecast of 2026 lentil plantings came in at 4.14 million acres, nearly 6% less than last year. In reality though, Canadian acreage of lentils has not fluctuated a lot in the last ten years, and this change would be relatively modest. Since StatCan’s survey, green lentil prices have not shown much movement while red lentil bids have firmed up a bit, which could add a few more acres by seeding time.

Over the past few years, green lentil prices have been at a large premium to reds, which caused a large shift into greens, especially in 2025. This winter though, red lentil bids are basically on par with large greens and well above small green lentil prices. As a result, we expect acreage to tip back toward red lentils. Over the past ten years, reds have accounted for two-thirds of Canadian lentil acreage but in 2025, that dropped to just under half. If the split between red and green lentil acreage gets closer to normal, it would mean a meaningful increase in red lentil acres while greens would drop considerably.

An average yield for lentils in 2026 would be 20 bu/acre, sharply lower than last year’s near record at 28.7 bu/acre and would have a much larger effect on the upcoming crop size than the drop in seeded area. If the yield slips back to average, lentil production would drop to 2.21 million tonnes, 34% smaller than last year’s crop of 3.36 million tonnes. Just like peas, this would help ease the heavy lentil supplies, especially greens, currently weighing on the market.

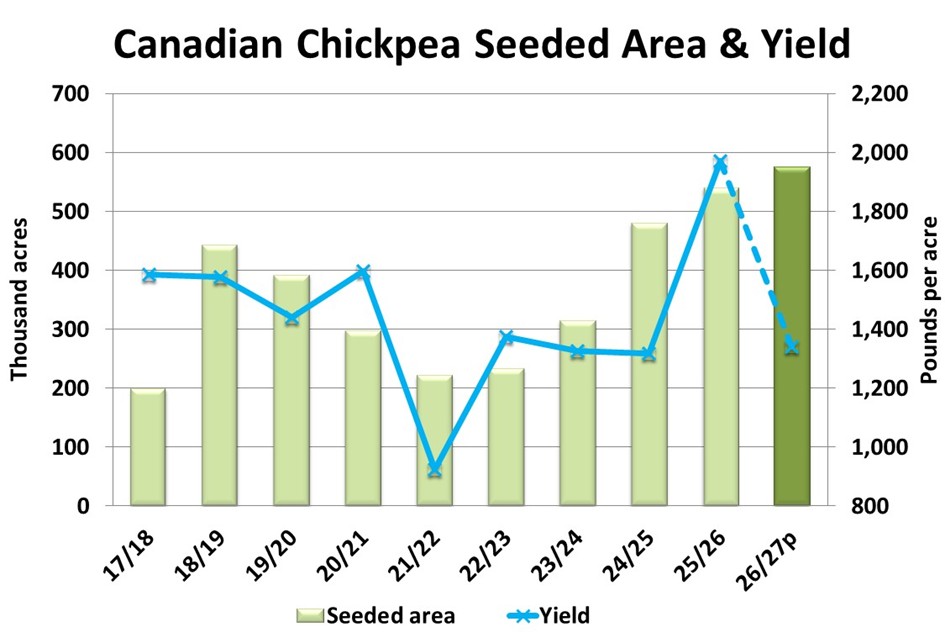

Chickpeas are the exception to other pulse crops, with StatCan showing an increase in 2026 acreage. Seeded area is forecast at 575,000 acres, the highest since the “chickpea bubble” way back in 2001/02. That acreage increase is forecast despite prices at multiyear lows, as kabuli chickpeas are still one of the better options in the brown soil zone.

Just like other pulses, chickpea yields in 2025 at 32.8 bu/acre were close to a record while the five-year average is more than 10 bushels lower. If the 2026 yield ends up close to that average, it would more than offset the acreage increase and production could be down 29%. The difficulty for the chickpea market though is that the old-crop carryover from 2025/26 will be very large and could potentially leave next year’s supplies at record levels.

The most debatable number in StatCan’s 2026 estimates is dry bean acreage, which was reported at 295,000 acres. Even though pinto and black bean bids are lower this year, this 31% drop in acreage seems overdone. That is especially the case as it is unlikely acres will drop to the lowest level since 2015. It is important to note that StatCan’s estimates for dry beans have often required sizable revisions, so this may not be the final word.

One final word: recent events in the Middle East are raising questions about last-minute changes to farmers’ planting decisions. While the impact on fertilizer prices is real, it may not have a large impact on pulse acreage. Looking back at 2022, when fertilizer prices were even higher, there was not a noticeable impact on pulse acreage; in fact, seeded area of peas that year was actually 500,000 acres lower than the previous year. In part, the effect of the higher fertilizer prices is probably muted because a good portion of farmers already locked in their pricing over the winter. That said, if fertilizer availability is impacted in a large way, some tweaking around the acreage margins is still possible.

Chuck Penner operates LeftField Commodity Research out of Winnipeg, MB. He can be reached at info@leftfieldcr.com.