By Chuck Penner, LeftField Commodity Research

December 2024

I was very saddened to hear about the recent passing of Peter Semmler, who provided Australian pulse outlooks for SPG. I appreciated our connections over the years, which were always very positive and helpful. I am honoured to try to fill in for Peter.

The Australian growing season has seen some big shifts in 2024/25, both for acreage and yields. The harvest is nearly complete for some pulse crops while it is still ongoing for others. At this stage, there are still plenty of questions about the outcomes. Part of the uncertainty is due to reservations about the acreage numbers from the Australian Bureau of Agricultural and Resource Economics (ABARES), Australia’s Ag Ministry – not much different than doubts about estimates from the United States Department of Agriculture (USDA), Statistics Canada (StatCan) and other countries’ organizations. Keep in mind that history shows ABARES’ pulse production estimates are frequently understated and often need to be revised higher to keep up with export totals.

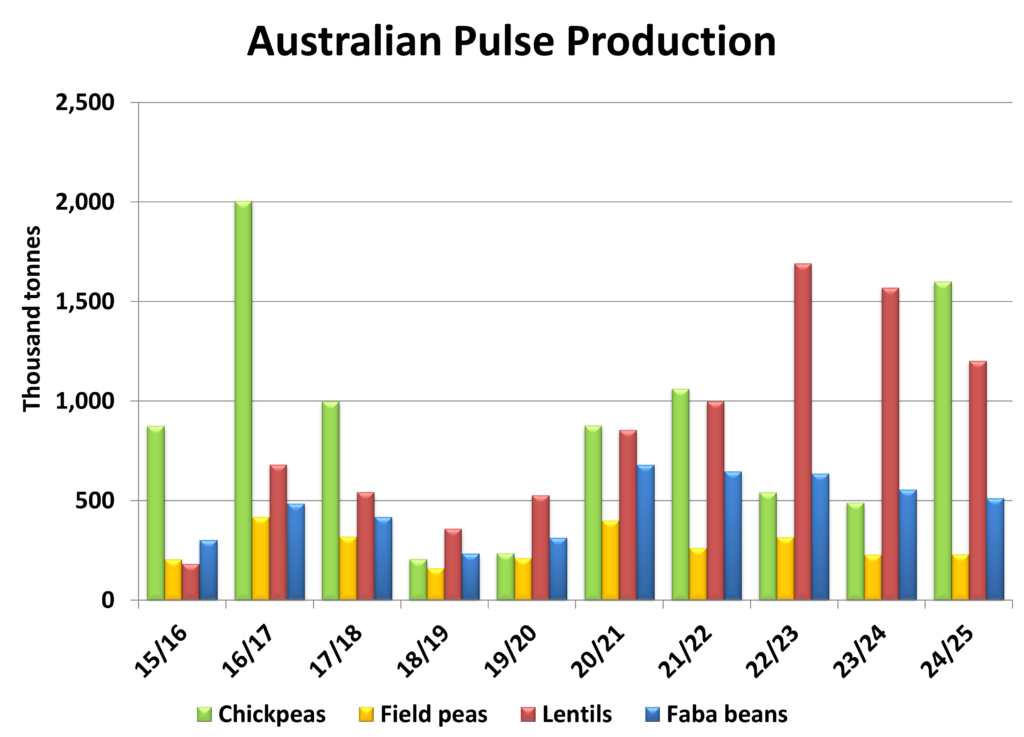

According to ABARES, Australian farmers boosted seeded area of chickpeas (mainly Desis) in 2024/25 to 769,000 hectares, 88% more than last year. Some other observers are saying acreage is even larger. While there were a few trouble spots, conditions in Queensland and New South Wales where chickpeas are grown were mostly very favourable.

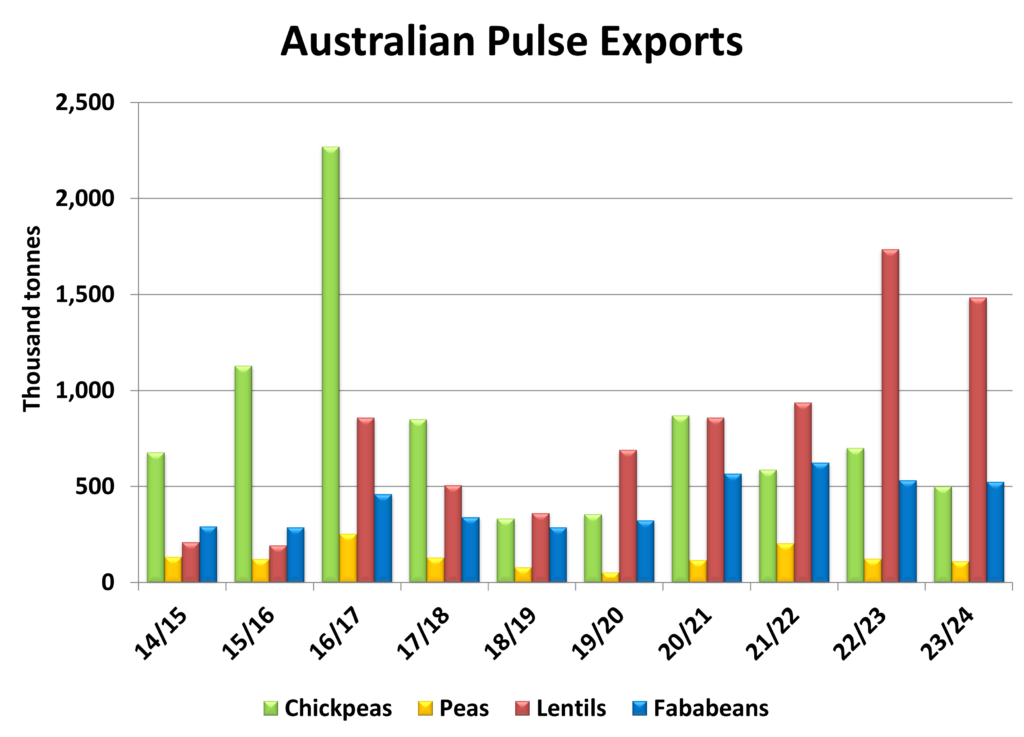

The chickpea harvest is now in its very late stages and anecdotal reports are talking about very positive yields. The last available production report from ABARES in early September reported the chickpea crop at 1.3 million tonnes while other private estimates are in the 1.5–1.7 million-tonne ballpark, and some even higher. Despite the wide range of estimates, it is clear this would be the second largest Australian chickpea crop on record. Keep in mind that trade data from Australia shows that over the past five years, chickpea exports have averaged 108% of production, indicating that crops have been underreported.

Australian chickpea exports dipped in 2023/24, mainly due to lack of supplies due to last year’s smaller crop. For 2024/25, there is very strong interest in Australian Desi chickpeas from South Asia, particularly India and Pakistan. Prices are off from last year’s highs, but the solid demand is still keeping prices fairly well supported.

There is also a wide range of ideas about the Australian lentil crop for 2024/25. Seeded area was reported by ABARES at 927,000 hectares, 17% more than last year, but some observers think that number is too low.

Most of the uncertainty for Australian lentils though is about yield prospects. In early September, just before frost hit key lentil-growing areas in Victoria and South Australia, ABARES estimated the crop at a near record 1.7 million tonnes. Some areas had already been experiencing drought conditions and the frost further damaged the crop. Right after the frost, a few crop estimates dropped as low as 1 million tonnes but now that the harvest is starting, some observers are expecting production closer to 1.2 million tonnes. Just as a reminder, over the past five years, Australian lentil exports have averaged 105% of production, confirming that the crop estimates from ABARES are underreported.

The pre-frost estimates of a record Australian lentil crop were raising ideas about a potential glut in red lentil supplies and prices in Australia had been dropping. The losses caused by the frost eased those concerns and Australian red lentil prices have rebounded from the earlier lows.

Seeded area of faba beans has been fairly steady in recent years and for 2024/25, ABARES estimated plantings at 259,000 hectares, nearly unchanged from last year. Most faba beans escaped damage from the September frost event and production further up the east coast is looking quite positive. In September, ABARES’ estimate of the faba bean crop was 511,000 tonnes, 8% less than last year, but that is likely the low end of the range.

Even with a smaller crop this year, Australia will still be the dominant exporter of faba beans into Egypt and other destinations in 2024/25. Interestingly though, faba bean prices in Australia have been rallying even as the harvest is ongoing, which suggests strong demand from importers. Based on the ABARES crop estimates and Australian trade data, over 90% of faba bean production is usually exported.

Peas are one of the smallest pulse crops in Australia, with seeded area estimated at 187,000 hectares, 3% less than last year. According to ABARES’ September report, the 2024/25 pea crop would come in at 230,000 tonnes, unchanged from the previous year. Other than 2021/22, when Canada’s pea crop was reduced by drought, Australian pea exports have averaged close to 100,000 tonnes, less than half of production.

There is one other possible wrinkle in the Australian crop situation: recent rains have disrupted the harvest in many areas. Most of the chickpea harvest was advanced enough to avoid any issues. For other pulse crops, there are not any confirmed reports of quality or yield losses due to the rain, but it is something to keep watching.

Chuck Penner operates LeftField Commodity Research out of Winnipeg, MB. He can be reached at info@leftfieldcr.com.