By Gaurav Jain, AgPulse Analytica

June 2026

Australia is entering the 2026 pulse season with one of the most divergent production outlooks in recent years. According to AgPulse Analytica’s latest 2026 Pulses Monthly report, a clear north-south weather divide is shaping the season: favourable moisture conditions in southern lentil regions versus persistent dryness in northern chickpea-growing areas of Queensland and New South Wales.

Chickpea Outlook

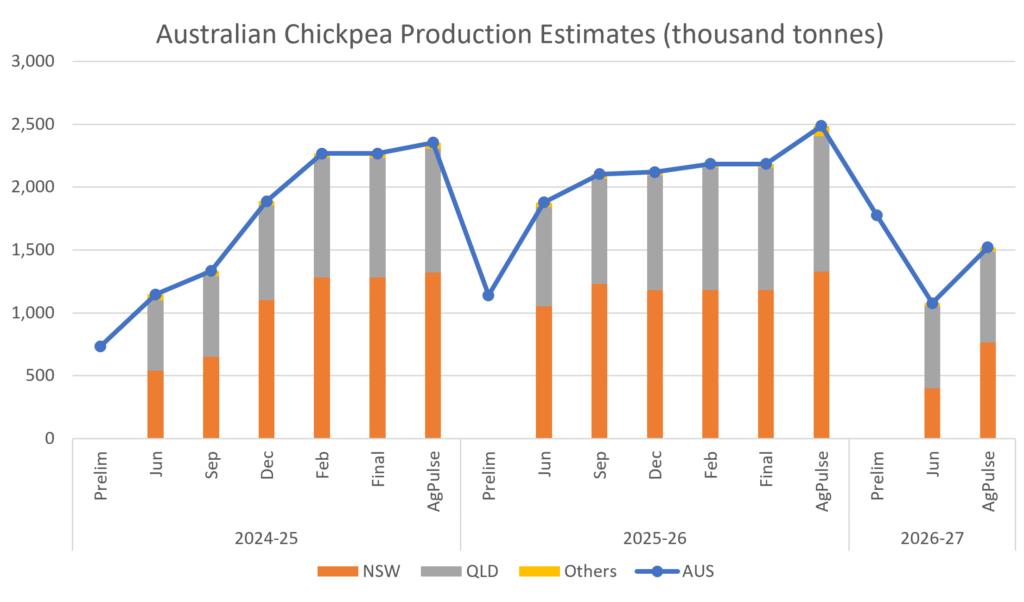

Desi chickpeas remain Australia’s flagship pulse export. The ongoing 2025/26 season delivered a strong 2.5 million tonne crop, supporting 2.25 million tonnes in exports and resulting in the ending stocks of 400,000 tonnes. However, sowing for the new season began under challenging dry soil conditions. Long-range forecasts point to a high probability of a strong El Niño development, with expectations the pattern could persist through much of 2026, threatening crop establishment and yields.

AgPulse Analytica outlines three distinct scenarios for 2026/27:

- In the pessimistic case (dryness continues, fewer acres, and poor yields), production collapses to just 1.13 million tonnes, slashing exportable surplus to 1.3 million tonnes and reducing ending stocks to a tight 100,000 tonnes.

- The realistic scenario (as per current short- and long-term forecasts) projects production at 1.50 million tonnes, with exports around 1.7 million tonnes and ending stocks at 130,000 tonnes.

- Only in the optimistic scenario (plenty of rain now and in September and weak El-Nino) does production recover strongly to 2.28 million tonnes, enabling exports up to 2.3 million tonnes.

Balance Sheet for Australian Chickpeas (thousand tonnes)

| (Oct – Sep) | 2024/25 | 2025/26 | 2026/27 | ||

| Pessimistic | Realistic | Optimistic | |||

| Area (thousand hectares) | 1,039 | 1,100 | 950 | 1,050 | 1,200 |

| Yield (tonnes/hectare) | 2.27 | 2.26 | 1.18 | 1.45 | 1.90 |

| Production | 2,354 | 2,486 | 1,125 | 1,520 | 2,280 |

| Carry-in Stocks | 84 | 251 | 398 | 398 | 398 |

| Imports | 1 | 1 | 1 | 1 | 1 |

| Total Supply | 2,439 | 2,738 | 1,524 | 1,919 | 2,679 |

| Domestic Use | 95 | 90 | 85 | 92 | 100 |

| Exports | 2,093 | 2,250 | 1,330 | 1,700 | 2,300 |

| Ending Stocks | 251 | 398 | 109 | 127 | 279 |

Table 1 Source: AgPulse Analytica Research

This uncertainty has made Australian growers reluctant sellers of old-crop stocks. Many are treating current inventories as strategic reserves rather than surplus, anticipating potential weather-related shortfalls later in the season. This has already resulted in a bullish market, despite pressure from the appreciating Australian Dollar.

Lentil Outlook

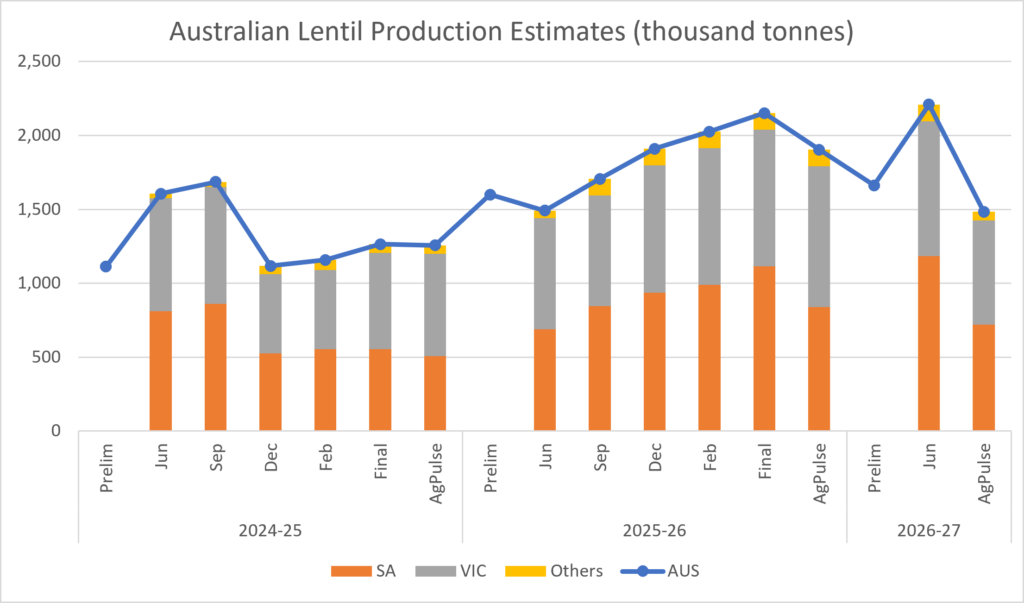

The story is markedly more positive for lentils. Southern growing regions in South Australia and Victoria have enjoyed excellent soil moisture and repeated rainfall events, creating highly conducive conditions for crop development.

AgPulse Analytica’s projections for 2026/27 reflect this:

- Pessimistic scenario (less rain in Aug-Sep and frost): Production falls to 1.25 million tonnes with exports at 1.2 million tonnes.

- Realistic scenario (current long-range forecasts): Production reaches 1.6 million tonnes, supporting exports of 1.4 million tonnes.

- Optimistic scenario (no frost and ample soil moisture throughout growing season): Output climbs to 1.78 million tonnes with exports returning to 1.6 million tonnes.

Balance Sheet for Australian Lentils (thousand tonnes)

| (Oct – Sep) | 2024/25 | 2025/26 | 2026/27 | ||

| Pessimistic | Realistic | Optimistic | |||

| Area (thousand hectares) | 1,020 | 1,130 | 850 | 1,000 | 1,100 |

| Yield (tonnes/hectare) | 1.23 | 1.69 | 1.47 | 1.60 | 1.62 |

| Production | 1,256 | 1,904 | 1,250 | 1,600 | 1,780 |

| Carry-in Stocks | 204 | 325 | 546 | 546 | 546 |

| Imports | 1 | 1 | 1 | 1 | 1 |

| Total Supply | 1,460 | 2,231 | 1,797 | 2,147 | 2,327 |

| Domestic Use | 80 | 85 | 75 | 85 | 90 |

| Exports | 1,055 | 1,600 | 1,200 | 1,400 | 1,600 |

| Ending Stocks | 325 | 546 | 522 | 662 | 637 |

Table 2 Source: AgPulse Analytica Research

Even in the realistic case, Australian lentils will add comfortable volumes to global supplies, likely maintaining downward pressure on prices amid already ample world stocks.

Global Trade Implications

This north-south split arrives at a pivotal time for international markets and the first crop report released by the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) validates it again. While chickpea crop for 2026/27 is estimated at just 1.1 million tonnes, lentil production is adjudged at a record 2.2 million tonnes.

South Asian demand continues to strengthen. India is expected to import a minimum of 1.1 million tonnes of desi chickpeas in 2026/27 (Apr-Mar) to fulfill its domestic demand. Pakistan’s total chickpea (desi and kabuli) import demand is projected at 750,000 tonnes in 2026, with Australia traditionally a leading supplier. Bangladesh also requires higher imports to meet Ramadan demand across two seasons.

For Canadian pulse exporters, the implications are significant and category-specific. A pessimistic or realistic Australian chickpea outcome would reduce global desi supply and ease competition in key South Asian markets, potentially opening import demand for its yellow peas and small caliber kabuli chickpeas supporting firmer prices and better export opportunities for Saskatchewan producers. In contrast, steady Australian lentil production under realistic or optimistic scenarios will keep that market competitive, requiring Canadian exporters to focus on quality differentiation and alternative destinations.

Overall, Australia’s 2026 season is not defined by absolute global shortage but by pronounced regional imbalance. How the weather evolves over the coming months will play a major role in reshaping pulse trade flows and creating both challenges and opportunities for Canadian exporters in the 2026/27 marketing year.

Gaurav Jain is the founder and chief analyst at AgPulse Analytica, based in New Delhi. He can be reached at gaurav@agpulse.net